July 13, 2023

This is a link to an article written by Nomaan Ilyas, published in the American Magazine in July 2023

This is a link to an article written by Nomaan Ilyas, published in the American Magazine in July 2023

The IRS recently released guidance on ‘non-fungible tokens’ (NFTs) and published their intent to issue guidance related to the taxation of certain NFTs as ‘collectibles’ in order to determine whether a gain from a sale of an NFT is taxed at the maximum capital gains tax rate of 28% or at a rate more favourable to assets that are not collectibles.

The IRS are looking to implement the ‘look-through rule’ to determine whether an NFT classifies as a collectible for US federal income tax purposes by looking through to the underlying associated right or asset, and use the results to state whether such ‘associated right or asset’ constitutes as a collectible; and therefore be taxed at a maximum of 28% if a capital gain were to be made at a sale.

If the IRS were to find, via the look-through rule, that an NFT does not classify as a collectible by analysing it’s underlying associated right or asset then the proceeds from the sale of such NFT will be subject to a maximum 20% long-term capital gain tax rate.

Please contact our team if you require further information.

For those of you who have considered renouncing your US citizenship may know that it has become ever more difficult to do so. A process that used to take a few months is now taking well over a year. Post covid, the US Embassy in London had only started to take requests for the renunciation interview last summer. There is no given time frame of when you will receive your appointment date, but we know it is taking longer than a year for the interview confirmation to come through. Due to this many who had considered renouncing their citizenship have since changed their mind. Others who are desperate to give up their citizenship have even considered travelling abroad to make an appointment with a US consular service that have a quicker turnaround.

There has however been some positive news for those still considering renunciation. Following the ongoing case against the US Department of State by the Paris based Association of Accidental Americans, the US state Department announced that it intends to reduce the fee is charges for renunciation to $450. The current fee is $2,350 and is the highest fee charged by any nation for the voluntary renunciation of citizenship, with some countries charging nothing for the right to expatriate. It is not yet clear when the change of fee will be implemented. Fabien Lehagre, founder, and president of the Association of Accidental Americans commented: “The State Department’s statement is extremely encouraging and tacitly acknowledges that this legal challenge has and will accomplish what it set out to do. By lowering the fee to $450, the U.S. government is showing that the right of voluntary expatriation is not to be trifled with and deserves the utmost protection. Time will tell how the government will formulate and develop the new fee and my organization intends to continue to campaign against any fee or restriction on this sacred right of renunciation.”

On 29 November 2022, Brazil and the UK signed a Double Taxation Agreement (DTA) which will enter into force when the relevant legislative procedures are completed. The DTA will establish the following withholding tax rates or source country taxation..

Dividends (Article 10):

10% of the gross number of dividends paid to a company (the beneficial owner) that holds directly at least 10% of the capital of the payer company throughout a period of 365 days. In all other cases, the rate will be 15%.

Interest (Article 11):

7% of the gross amount of interest paid to a bank or insurance company on a loan that was granted for at least a five-year period to finance infrastructure projects and public utilities.

10% of the gross amount of interest from: loans granted by banks, bonds that are regularly traded on a qualified stock exchange and a sale on credit paid by the purchaser of equipment to the seller.

For all other cases, the rate will be 15%.

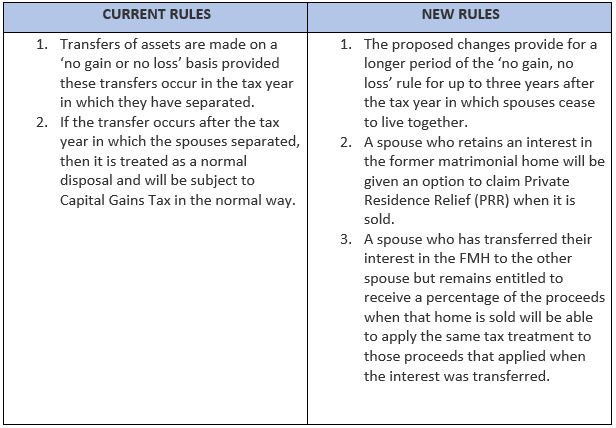

In 2021, The Office of Tax Simplification (OTS) reviewed the current CGT rules relating to separating couples or civil partners and proposed a number of recommendations which have been accepted by the Government, although is yet to be progressed through Parliament.

This proposal has come into light as at present, no capital gains tax (CGT) is charged on a transfer of assets between a married couple or civil partners who live together. However, if the couple separate or divorce, this tax relief does not necessarily apply.

The new rules intend to enable a couple to separate and divorce without undue pressure to reach a financial agreement due to CGT consequences.

The Chancellor of the Exchequer, Jeremy Hunt, announced significant changes to the personal tax code for pensions.

The Changes taking place from April 6th, 2023:

Annual Allowance (AA) – will rise from £40,000 to £60,000 annually.

Money Purchase Annual Allowance (MPAA) and Tapers Annual Allowance (TAA) will rise from £4,000 to £10,000 per year.

Lifetime Allowance (LTA). LTA will be completely abolished in a future finance Bill.

Pensions Commencement Lump Sum (PCLS). The maximum PCLS for individuals without protections will remain at 25% of the current LTA (£268,275) and will then be frozen.

What are the effects of the changes on individuals?

In its most recent Pension Schemes Newsletter, HMRC clarified the situation, stating that participants with active enhanced or fixed safeguards will be able to accrue new benefits, join other programmes, or move without losing such protections if the application was made by 15 March 2023. Members who have a protected right to a higher PCLS will continue to have that privilege. Despite this, there are still a lot of unanswered concerns, especially around what a Labour government might accomplish.

What are the effects of the changes on employers and trustees?

While the announcements of the Chancellor’s reforms will be welcome news for some, the unanswered questions will leave many wary. Pensions is a long-term financial planning tool, so individuals need reliable and consistent rules in order to plan effectively. Ultimately, the devil will be in the detail. Some (but not all) of that will be introduced in future Finance Bills, and (relative) certainty may not be achieved until after the next general election.

HMRC has increased the interest rate it charges on unpaid income tax, national insurance, capital gains tax, stamp duty, corporation tax and inheritance tax to 6.75% following last month’s Bank of England base rate rise. The rate now stands at a 14-year high and is more than double what it was last January, when it was 2.75%.

However, those owed money by HMRC will receive just 3.25% interest, up more than two percentage points since January last year. The interest rate on late paid tax has doubled in less than a year therefore delaying paying HMRC has a real cost to it. Therefore, If you are going to struggle to pay your bill on time, agreeing a formal time to pay arrangement with HMRC before the penalty is charged will mean as long as you stick to the instalment payments agreed, the penalty won’t be charged. However, interest will be applied.

Chancellor Jeremy Hunt presented a “Budget for Growth”, after the Office for Budget Responsibility predicted that the UK economy will perform better than expected this year with inflation continuing to fall. We have summarised the changes that were outlined and we hope this will help you to better understand the UK’s current position. Here are some key points to note:

• Tax on dividends, where taxable, will increase by 1.25% from 6 April 2023.

• The Annual Allowance for pensions has increased from £40,000 to £60,000.

• The pensions Lifetime Allowance charge abolished.

• Limitations to the maximum an individual can claim as a Pension Commencement Lump Sum to 25% of the current Lifetime Allowance (£268,275), except where previous protections apply.

• The expected increase in the rate of corporation tax for many companies from April 2023 to 25% will go ahead.

• From April 2023, companies will be able to raise up to £250,000 of Seed Enterprise Investment Scheme (SEIS) investment, a two-thirds increase.

• The annual investor limit will be doubled to £200,000 for SEIS.

• No changes to the current rates of CGT have been announced.

• Inheritance Tax nil-rate bands will remain fixed until April 2028.

You can view our summary HERE and if you have any questions feel free to contact us.

As you may already be aware, offshore entities which own UK property needed to register on the Register of Overseas Entities (“ROE”) before the deadline on January 31st, 2023. HMRC will use the information submitted to investigate any arrangements which they suspect have failed to comply with their UK tax obligations.

However – taxpayers still have time to submit a disclosure should they feel that they have not paid the correct amount of tax in respect to a UK property; HMRC has allowed taxpayers until February 28th, 2023 to inform them that a disclosure will be submitted which may reduce any penalties charged.

The penalty regime for not notifying HMRC of taxable offshore income, assets or activities could potentially be severe and where unpaid tax exceeds £25,000, imprisonment of up to 51 weeks and an unlimited fine may be applicable, irrespectively of whether tax evasion was intentional.

The State of Massachusetts have recently approved a 4% tax on annual income above $1 million, on top of the State’s current 5% flat income tax rate. The additional tax has become effective from January 1, 2023. Although this tax will only apply to around 0.6% of Massachusetts households, it is estimated that the levy will bring in roughly 1.3 billion in revenue during 2023. The aim is to use the additional tax to fund public education, roads, bridges, and public transport.

Since the announcement, many high earners in Massachusetts have already put a number of plans in place such as accelerating their income into 2022 if at all possible. This would include accelerating receipt of deferred compensation or selling as asset before the new levy comes into effect. Some have opted to spread their income over a number of years to stay below the $1 million threshold.

Some are even considering moving. As a final option higher earners may choose to leave Massachusetts and opt to live and work in a lower tax State. Although a big step, this may be the only option for some and worthwhile if the levy means a huge tax increase for them.

California State recently rejected a similar proposal of a 1.75% on annual income of more than $2 million, where the funds were earmarked for zero emission vehicle subsidies. California already has a much higher rate of tax of 13.3% for those earning over $1 million. So, has a State trend begun? Experts do not believe there is a broader trend at State level of a millionaire tax rate, as most States have actually reduced their tax rates for 2023. However, this is something to keep an eye on.