| The Internal Revenue Service (IRS) expects to issue final regulations under Section 401(a)(9) of the Internal Revenue Code for determining required minimum distributions (RMDs) beginning in 2025. Until then, the IRS has extended the relief previously provided to defined contribution plans and beneficiaries for certain required minimum distributions (RMD) failures by issuing Notice 2024-35

Qualified plans are required to make RMDs to participants by their required beginning date. Plans are also required to make RMDs to beneficiaries if the participant dies before his or her required beginning date. Prior to passage of the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE 1.0), if a participant died before his or her RMDs began, the participant’s entire benefit generally had to be distributed to his or her beneficiary either within five years after the participant’s death, or over the life or life expectancy of the participant’s designated non-spouse beneficiary. These two payment rules are commonly referred to, respectively, as the “five-year rule” and the “life-expectancy rule,” with special rules applying if the participant’s beneficiary is the surviving spouse. Distributions under the five-year rule generally could be delayed until the end of the five-year period, whereas distributions under the life-expectancy rule were required to begin no later than one year after the participant’s death. In addition to increasing the RMD age from age 70.5 to age 72, SECURE 1.0 eliminated post-death distributions under the life expectancy rule for most defined contribution plan beneficiaries. Rather than stretching post-death distributions under the life-expectancy rule, SECURE 1.0 generally requires defined contribution plans to distribute a participant’s entire benefit within 10 years after the participant’s death. This payment rule applies for participants who die after December 31, 2019. SECURE 1.0 includes an exception to the 10-year rule for beneficiaries who qualify as eligible designated beneficiaries, as defined under the code. The IRS issued proposed RMD regulations in 2022 to implement the SECURE 1.0 changes. Unlike the pre-SECURE Act five-year rule, however, the proposed regulations generally require RMDs under the 10-year rule to begin the year after the participant’s death. Because under the 5-year rule beneficiaries could delay RMDs until the end of the five-year period. They were surprised by the RMD commencement requirement under the 10-year rule and expressed concerns during the regulatory comment period about the timeliness of RMDs under the 10-year rule. The IRS previously issued Notice 2022-53 and Notice 2023-54 in response to these concerns. Under the notices, the IRS provided temporary relief to defined contribution plans and beneficiaries in connection with RMD failures under the 10-year rule for distributions that should have been made in 2020 through 2023. By issuing Notice 2024-35, the IRS has extended this relief to RMDs that should have been paid to beneficiaries under the 10-year rule in 2024. As a result, the IRS will not treat defined contribution plans as failing to satisfy Code Section 401(a)(9) and will not assert an excise tax on beneficiaries for RMDs that should have been paid under the 10-year rule in 2020 through 2024. |

| Frontier Group Mermaid House 2 Puddle Dock London EC4V 3DB |

Telephone: + 44 (0) 207 332 2810 Fax: +44 (0) 207 332 2984 Email: info@frontier-fs.com |

| © Frontier Group. All Rights Reserved. Unsubscribe from this newsletter |

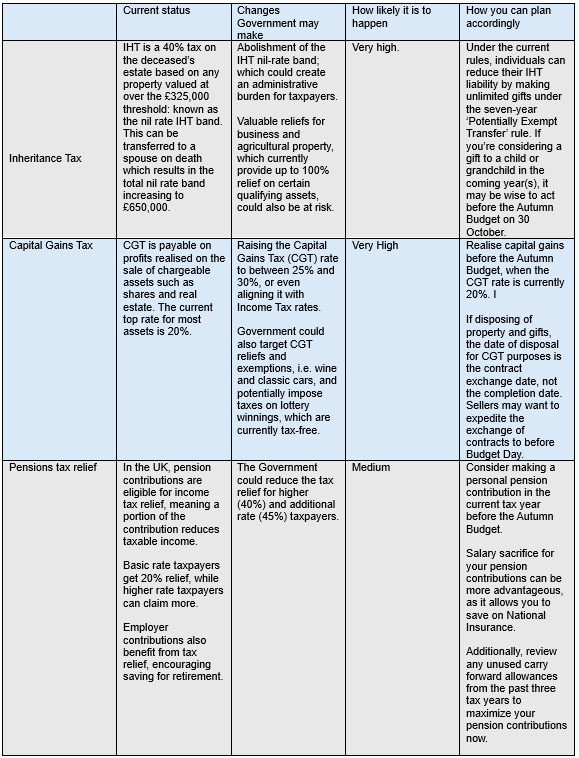

With the new Labour government in charge, we know that there will be further changes to non-UK Trusts in addition to what the conservatives had proposed. I have detailed the key aspects below.

- Labour have indicated there would be no grandfathering of existing trusts. At this stage, it is safe to assume that even existing excluded property trusts will no longer benefit from IHT protection from April 2025.

- If the settlor is a long-term UK resident and also a beneficiary of the trust, then not only will trust assets become subject to periodic IHT charges but they will also form part of the settlor’s estate on death and therefore subject to inheritance tax at 40%. This is a very significant change and could have enormous implications for many trusts, particularly where the settlor is older or in poor health and so the risk is greater.

- Regarding income tax and capital gains tax, from 6 April 2025, foreign income and gains within trusts will be taxable on the settlor on an arising basis as if they owned the trust assets personally.

- Serious consideration should now be given to whether the settlor can afford to give up being a beneficiary of the trust.

- Ideally, any planning steps would be deferred until after draft legislation has been published. However, given the potentially significant tax implications, the trustees and the settlor may not have the luxury of waiting.

- Any restructuring implemented after Labour’s first budget, likely to be in September, may be too late if anti-forestalling measures are announced.

- Additionally for any non-doms with personal assets, they should consider steps they need to take to put themselves into a better tax position.

Please let us know if you would like to discuss any of these issues.

A non-dom businessman fell foul of the complex remittance basis rules. However, errors by HMRC rendered their discovery assessment invalid and saved the taxpayer a sizeable proportion of the tax.

In Afzal Alimahomed vs HMRC [2024] UKFTT (TC) 432, it was not in dispute that the transactions in question related to foreign income and gains. Therefore, the issue of whether income had been remitted was central to Alimahomed’s dispute with HMRC.

Alimahomed had transferred sums from an Isle of Man bank account to his son, a university student in the UK at the time. He made further bank transfers directly to his son’s university and landlord in respect of his son’s tuition and accommodation expenses. He argued that Condition A of section 809L Income Tax Act 2007 was not satisfied because he had not brought money into the UK, for two reasons.

First, a bank transfer is not legally a transfer of money. Instead, there is a debit against Alimahomed’s account and a corresponding credit in the recipient’s account. From a legal perspective, nothing had been transferred. Secondly, by initiating a bank transfer, Alimahomed had not brought money to the UK but had simply sent it to the UK, which fell outside the statutory definition.

Given these submissions would exclude all bank transfers from being taxable on the remittance basis, it is unsurprising that the first tier tribunal (FTT) disagreed. It held that bringing money to the UK includes executing the transfer or transmission of money by electronic bank transfer.

Alimahomed paid his son’s university and accommodation expenses, and purchased various items of jewellery, using a Dubai credit card. The balance of that card was paid from an account that contained overseas income and capital gains.

Under section 809L, the payment of the balance is only taxable as a remittance if it is a “relevant debt”, meaning that the debt relates to property received in the UK or services provided in the UK to or for the benefit of Alimahomed.

The taxpayer argued that any enjoyment of the services or property in the UK was by other people and therefore the credit card balance was not a relevant debt. Again, the FTT rejected his arguments, although its reasoning appears to contain a significant omission.

The FTT held that the use of a credit card to make purchases of any property in the UK creates a relevant debt, which is sufficient to dispose of the various gifts. With respect to the services, the FTT’s reasoning is thin. It concluded that, by paying for them, Alimahomed must have created a relevant debt. It does not address the requirement in section 809L that the services must be provided to or for the benefit of Alimahomed or explain how this requirement is satisfied.

Finally, Alimahomed attempted to argue that the jewellery he had purchased for himself, and his wife was exempt property under section 809X ITA 2007 because they were items for personal use. The FTT held that the exemption had no application where it is the satisfaction of the credit card debt which amounted to a remittance.

Alimahomed argued that the discovery assessment in relation to the 2015/16 tax year was invalid because HMRC had failed to prove their case. This was irrelevant in respect of the 2016/17 tax year, which was dealt with by issuing a closure notice.

HMRC is required to prove that a discovery assessment was validly issued in accordance with section 29 TMA 1970. In their statement of case, HMRC alleged that the discovery assessment was valid because the loss of tax had been brought about deliberately by Alimahomed.

In the hearing, HMRC abandoned that argument but made no formal application to amend its statement of case. The FTT held that HMRC could not depart from the case it had originally set out and had failed to demonstrate the validity of the discovery assessment. Therefore, the appeal was partially allowed in respect of the discovery assessment, worth just under £90,000.

Non-doms will need to be careful to avoid inadvertent remittances creating accidental tax charges.

Benoît d’Angelin, a non-domiciled investment banker originally from France and currently residing in Italy, has lost his appeal against a £675,000 tax bill in the UK. Despite legal advice that his £1.5 million investment in his UK company, d’Angelin & Co, would qualify for business investment relief, HMRC deemed his use of director loans for personal expenses as a breach of tax provisions.

Case Background:

– In 2016, d’Angelin, a UK resident but not domiciled, invested £1.5 million of his foreign income into his UK company, intending to benefit from business investment relief.

– He used a director’s loan account for £75,000 in personal expenses, including private jet hire, a 79p iTunes subscription, and gifts for his wife.

HMRC’s Position:

– HMRC argued that these personal expenses violated the “remittance basis” provisions of the Income Tax Act 2007.

– Consequently, the entire £1.5 million investment was deemed taxable, leading to a £675,000 tax bill.

Legal Proceedings:

– A closure notice was issued in June 2022, and d’Angelin appealed in November 2022.

– A penalty assessment of £101,295 for late payment of 2018/19 taxes was issued but later cancelled by HMRC due to an error.

Arguments and Judgment:

– d’Angelin’s representative, Michael Firth KC, contended that the extraction of value rule should refer to net value, and that the director’s loan was a standard business practice.

– HMRC maintained that any personal expense covered by the company constitutes a breach.

– Tribunal judge Christopher McNall agreed with HMRC, emphasizing that the purpose of the rule is to restrict foreign income usage strictly.

Conclusion:

– The tribunal concluded that d’Angelin’s actions were exactly what the extraction of value rule aims to prevent, leading to the loss of relief.

– The appeal was dismissed, leaving d’Angelin liable for the full £675,000 tax bill.

d’Angelin’s belief that his method was standard within his industry was acknowledged but ultimately insufficient to overturn the decision. Despite being advised of potential risks by his legal advisors, the tribunal found no grounds to exempt him from the tax liability.

Following the General Election, Labour now have a majority government with over 400 seats. There has been much speculation in recent months, since the spring Budget back in March, regarding potential changes in taxation.

Rachel Reeves, the new chancellor, is expected to announce the date of her first Budget by the end of July. Given the preparation time required and notice for the Office of Budget Responsibility (OBR) it is likely that the Budget would not be before October 2024.

Labour, so far, have ruled out Income Tax, National Insurance and VAT increases, however are expected to keep income tax thresholds frozen until April 2028. There has been no commitment to keeping capital gains taxes at the current level.

At the last Budget, the Conservatives outlined their proposals for Non-Dom and Inheritance Tax Reform – please see the following links for our coverage on this and the Labour comments:

There are other updates expected which will impact: Corporation Taxes (Labour has promised to cap this at 25%), Stamp Duty Land Tax (SDLT) for non-UK residents, along with a tightening of the tax rules for carried interest arrangements and potentially removing the VAT exemption for private school fees.

We will be closely monitoring any developments and will provide updates accordingly.

Please reach out to your usual Frontier contact if you would like to discuss how the above may impact your affairs.

Click below to view the article –

The UK will be heading to the polls on 4 July 2024 as the Government announced the early General Election. There are many who have been closely monitoring the situation for updates on the potential tax implications particularly for non-domiciled individuals.

Following the Budget back in March – please see the following link for our initial summary of the Conservatives announced changes due to come into force from 5 April 2025.

Labour issued a response to these changes back in April – the main differences in stance are as follows:

- Consider incentives for new arrivers to invest in the UK

- Want to adapt the plans for the transitional relief

- Not implement the 50% discount on foreign income remitted during 2025/26

- Not allow grandfathering of excluded property trusts set up before 6 April 2025

The comments from Labour are useful to obtain a sense of the intentions, however with no technical explanation the brief statement does not provide full clarity. Specifically regarding the treatment of excluded property trusts set up pre-April 2025, this would be very challenging to achieve through legislation given the complexities that arise with offshore settlements.

The impact of the early General Election is there will not be any draft legislation published this summer as originally expected and the consultation on the proposed inheritance tax changes will also be delayed.

At this stage, both the Conservatives and Labour have committed to non-dom reform in one version or another which means we can be fairly confident that there will be upcoming changes. Providing there is a clear majority in the election we will know which version is likely to be implemented; the uncertainty lies in the timing and effective date.

Once the Government session resumes, the main possibilities are as follows:

- An Autumn Budget is announced and will confirm the reforms – although this would leave the Government very little time to prepare draft legislation and the planned IHT consultation.

- The changes will be confirmed in a Spring Budget for 2025.

- The changes may be postponed for longer whilst legislation is drafted and consultations undertaken.

If history has any lessons, it cannot be guaranteed that either party would implement the changes in full as announced, however it would be prudent to assume this will be the case until the position is clear.

Should you wish to discuss the potential impact for your affairs please do reach out to your usual Frontier contact and we will be happy to discuss this with you

We bring to your attention the latest warning from the Internal Revenue Service (IRS) regarding fake charities and tax-related identity fraud. This advisory is part of the ongoing “Dirty Dozen” tax scams series, emphasizing the importance of vigilance and caution, particularly during times of natural disasters and tragic events.

Key Points:

- Scammers often exploit tragic events by posing as charitable organizations to solicit donations. They may also seek sensitive personal and financial information under the guise of charity work.

- Taxpayers should be aware that deductions for charitable donations are only valid when directed towards IRS-recognized tax-exempt organizations. Utilizing the Tax-Exempt Organization Search (TEOS) tool on IRS.gov can help verify the legitimacy of charities.

- Tactics employed by scammers may include email phishing, spoofed caller IDs, and targeting vulnerable groups such as seniors and individuals with limited English proficiency.

How to Protect Yourself:

- Refrain from making payments under pressure and avoid charities that request gift card numbers or wire transfers.

- Verify the legitimacy of any charity before making donations and avoid sharing excessive personal information.

- Report abusive tax practices and incorrect tax filings by using the online Form 14242 or submitting a completed paper Form 14242 to the IRS Lead Development Center.

It’s crucial to remain vigilant and informed about potential scams, especially those targeting charitable giving and tax-related identity fraud. By following the IRS guidelines and exercising caution, we can collectively combat fraudulent activities and protect ourselves and our communities.

State taxes can be confusing for US expats that are living abroad. Many will ask ‘Do I need to pay State taxes even though I am living abroad? The answer to this, unfortunately, is not black and white.

Each US State has different rules as to who qualifies as a state resident and what type of income would be taxable in that State. Some States have no income tax charges, such as Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming. Other States will have varying rules and if you have any affiliation to these States, such as you lived there before moving abroad, you have some workdays there, or you own a property there, it is important to understand the rules and check how they may apply to you.

For example, in some States if you are considered domiciled in the state, you could still be liable to State taxes even though you are not physically present there. In some States you could be liable to State taxes by travelling to and working within the State, even if this is just a few days. This would include remote working from a home you may still maintain within the State. If you are unsure if any of the State income tax rules will apply to you, please contact our team and they will be happy to assist you.